Heads Up for the 2020 Proxy Season: ISS Survey Results May Signal Policy Changes

Contributor(s)

|

|

|

Heads Up for the 2020 Proxy Season: ISS Survey Results May Signal Policy Changes

Contributor(s)

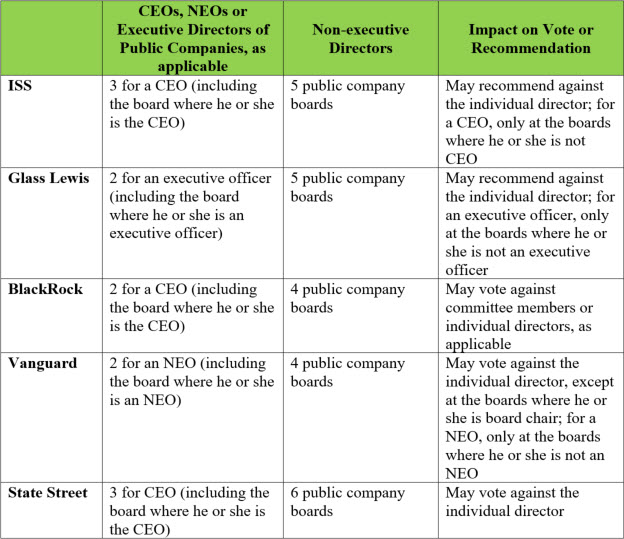

ISS has released results of its Governance Principles Survey which is often a precursor to changes to its voting policies. The results primarily reflect the views of U.S. institutional investors and public companies and are available here.1 We expect that ISS will publish draft 2020 policy updates in late October and release final policy updates in mid-November after a comment period. Key takeaways from the survey are as follows:

Director Overboarding (Global). Citing the “evolving views” of some large institutional investors, such as BlackRock, Vanguard and State Street that have adopted more restrictive policies, available here, here and here, ISS included a survey question on how many boards is too many for an individual director. At a glance, under the current applicable policies, the maximum number of boards on which directors may serve is as follows:  Investors tended to support four total board seats for non-executive directors (42%) and two total board seats for CEO directors (i.e., the CEO serves on one outside board in addition to his or her company’s board) (45%) as the appropriate maximum limit. Non-investors responded that the overboarding policy should not include a general limit for non-executive directors (39%) or CEOs (36%) but the board should consider what is appropriate and act accordingly. Although a significant number of non-investors (39%) expressed a preference for companies to set their own limits on the maximum number of director’s public company board seats, a greater percentage of non-investors (48% for non-executive directors and 57% for CEOs) favored some form of pre-established limit ranging from four to six total boards. Accountability For Climate Change Risk (Global). Investors and non-investors agree that companies should consider climate change risk. Only 5% of investors and 11% of non-investors responded that possible risks related to climate change are often too uncertain to incorporate into a company-specific risk assessment model. 60% of investors and 21% of non-investors supported the view that companies should be assessing and disclosing their climate-related risks and taking actions to mitigate them where possible. 35% of investors and 68% of non-investors preferred that each company determine the appropriate level of disclosure and action depending on a variety of factors, including its own business model, its industry sector, where and how it operates, and other company-specific factors and board members. Both investors and non-investors generally agree that engagement with the board and/or management and support of shareholder proposals seeking increased greenhouse gas (GHG) emissions or other climate-related measures are the most appropriate actions for shareholders to take at a company that is not effectively reporting on or addressing its climate change risk. Combined Chair and CEO Roles (U.S.). Citing the ongoing debate on whether independent board leadership is essential or whether a lead independent director is an acceptable alternative to an independent board chair, ISS asked what factors or circumstances would most strongly suggest the need for an independent board chair. Investors and non-investors generally agree that the most significant factors to consider would be: poor responsiveness to shareholder concerns, a weak or poorly-defined lead director role, governance practices that weaken or reduce board accountability to shareholders (e.g., a classified board, plurality vote standard, inability of shareholders to call a special meeting, lack of proxy access right) and a corporate crisis (e.g. a serious regulatory scandal, security breach, accounting scandal, or product/operational failure). Sunset Provisions for Multi-Class Stock (U.S.). In response to several recent multi-class structure IPOs, for the third year in a row, ISS solicited respondents’ views on what period of time is appropriate for a time-based sunset provision to be triggered for multi-class capital structures with unequal voting rights. Investors (55%) were more likely than non-investors (47%) to respond that a maximum seven-year sunset provision would be appropriate. Among respondents who did not find seven-years to be sufficient, 36% of non-investors favored ten years or more, while 35% of investors responded that no multi-class structure would be appropriate, regardless of the sunset provision. EVA Pay-for-Performance (U.S.). In 2019, ISS began to include additional information on company performance through the Economic Value Added (EVA) framework that applies a series of rules-based adjustments to financial statement accounting data offering a “uniform” non-GAAP basis for evaluating performance across companies. ISS intends to incorporate EVA metrics into the Financial Performance Assessment (FPA) screens, its secondary pay-for-performance screens, that is used to asses a narrow subset of companies where the primary pay-for-performance screens indicate a borderline result between Low and Medium concern levels. An overwhelming majority of respondents (84% investors and 71% non-investors) agreed that prior-used GAAP-based metrics should be displayed below the FPA screens as a point of comparison. Endnotes (≈ returns to text)

Contributor(s)

Co-Head of Governance, Securities & Reporting Group

More from the Governance & Securities Watch

Copyright © 2026 Weil, Gotshal & Manges LLP, All Rights Reserved. The contents of this website may contain attorney advertising under the laws of various states. Prior results do not guarantee a similar outcome. Weil, Gotshal & Manges LLP is headquartered in New York and has office locations in Austin, Boston, Brussels, Dallas, Frankfurt, Hong Kong, Houston, London, Los Angeles, Miami, Munich, New York, Paris, San Francisco, Silicon Valley and Washington, D.C.

|